The Pass-Through Entity (PTE) elective tax remains available in California and has been extended through 2030 but there are important updates for the 2026 tax year that business owners should know.

What the PTE elective tax does

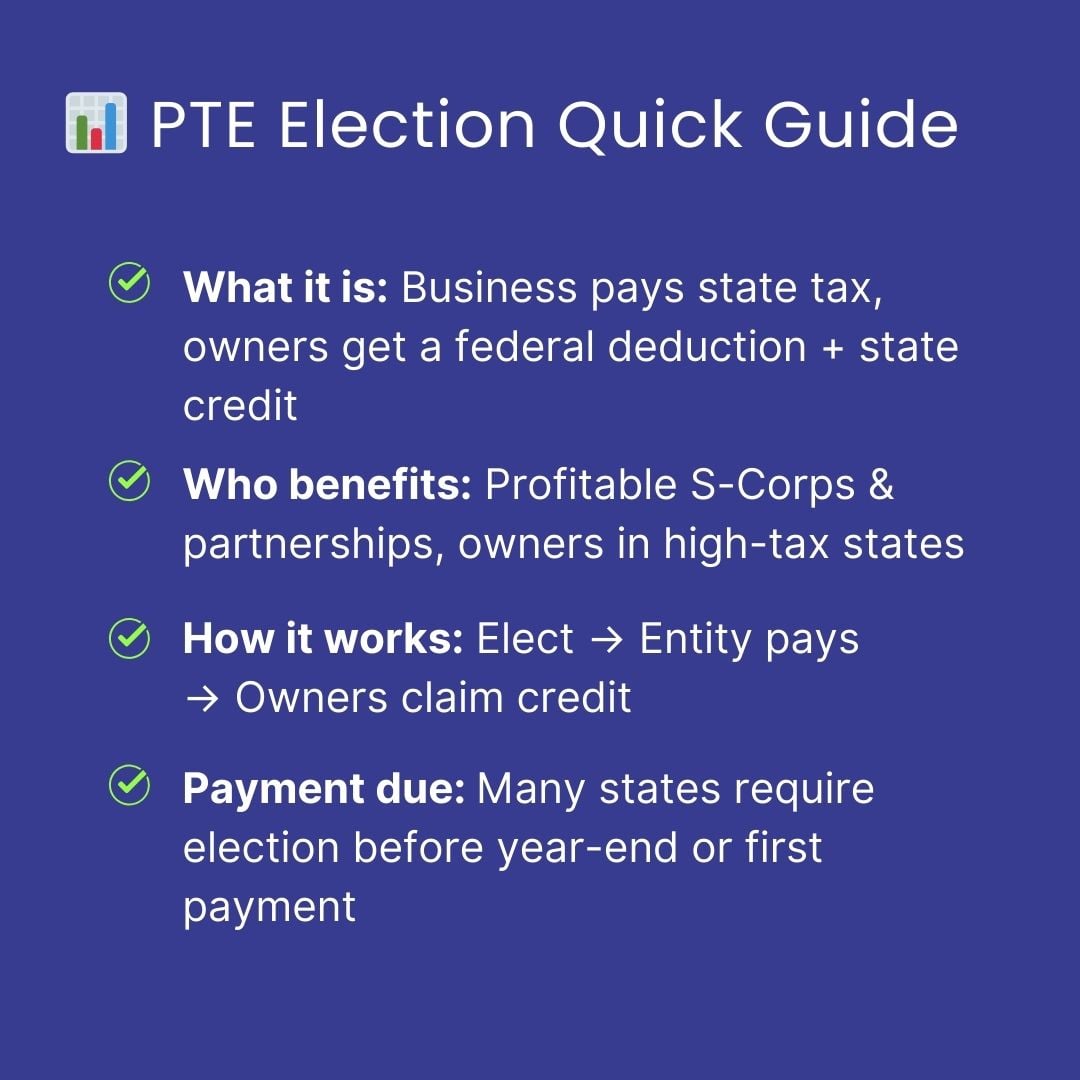

California’s PTE elective tax is imposed at a flat 9.3% on qualified net income. It allows certain pass-through businesses to pay California income tax at the entity level instead of the owner level. Owners then receive a state tax credit for their share of the tax paid, which can help reduce overall tax exposure.

Key deadlines this year (and where to pay):

June 15, 2026 – First Payment

- $1,000 or,

- 50% of last year’s PTE tax (whichever is higher)

Final payment: Due with the entity’s original return

For most calendar-year S-corps and partnerships, this is March 15, 2027 (or the next business day if the date falls on a weekend or holiday)

Pay online through the California Franchise Tax Board Web Pay or using Form FTB 3893 voucher

Owner credit:

- Claimed on the owner’s California personal return (Form 540)

- Unused credits can carry forward up to 5 years

What’s new in 2026

Before, missing the June payment could invalidate the elective tax entirely.

Starting in 2026:

- The elective tax can still be made even if the June payment is missed

- However, the credit may be reduced

Bottom line: you still benefit most by paying on time.

Who qualifies?

🟢 Eligible:

- S-corporations

- Partnerships

- LLCs taxed as partnerships

🔴 Not eligible:

- Sole proprietors

- C-corporations

- Publicly traded partnerships

- Entities in combined reporting groups

All participating owners must consent to the elective tax each year.

Final note

Deadlines and eligibility rules can change, especially when dates fall on weekends or holidays. We recommend confirming details with the California Franchise Tax Board.

If your business operates in multiple states, keep in mind that PTE rules, tax rates, and credit treatment vary widely by state, so each jurisdiction should be reviewed separately.